Finding yourself in a car accident is a stressful, disorienting experience. The adrenaline, the confusion, and the immediate concern for personal safety can sometimes cause even the most prepared drivers to forget the critical step of exchanging insurance and contact information with the other party. Whether due to an emergency, a language barrier, or a simple lapse in judgment, leaving the scene without this data can feel like a disaster.

However, the reality is that filing an insurance claim without the other party’s details is possible—though it certainly requires more diligence, patience, and documentation. Below, we break down the process, the risks, and the strategic steps you must take to protect your financial interests.

The Reality of Filing Without Information: Initial Steps

If you failed to exchange information at the scene, your first instinct might be panic. However, your insurance provider is experienced in handling "hit-and-run" or "unidentified driver" scenarios.

1. Notify Your Insurer Immediately

Do not wait. Even if you are unsure if you will file a formal claim, contact your insurance company as soon as possible. Delaying notification can sometimes be viewed as a violation of your policy’s "duty to cooperate," which could jeopardize your coverage. Provide them with a full, honest account of what happened, where it happened, and why you were unable to obtain the other party’s details.

2. File a Police Report

A police report is the cornerstone of your claim in these circumstances. It serves as an objective, third-party record of the event. Even if the police did not arrive at the scene, go to the nearest station to file a report. Include the location, time, and a detailed description of the other vehicle (make, model, color, and any partial license plate numbers). This document is often required by insurers to verify that the accident occurred and to establish that you did not simply invent the damage to your car.

3. Document the Scene Independently

If you are still in the vicinity of the accident or can return safely, gather evidence. Look for security cameras on nearby businesses or homes that might have captured the incident. If there were witnesses, try to obtain their contact information. This evidence is vital for your insurance adjuster to determine liability, especially if you intend to use your collision or uninsured motorist coverage.

Chronology: What to Do in the 48 Hours Post-Accident

To manage the situation effectively, follow this timeline to ensure your claim process is as "clean" as possible.

- 0–6 Hours: Prioritize medical safety. Once you are safe, report the incident to the police. The longer you wait, the less credible your account may seem to an insurance investigator.

- 6–24 Hours: Review your policy. Determine if you have "Uninsured Motorist Property Damage" (UMPD) or "Collision" coverage. These are the specific portions of your policy that will likely cover repairs when the other driver is unknown.

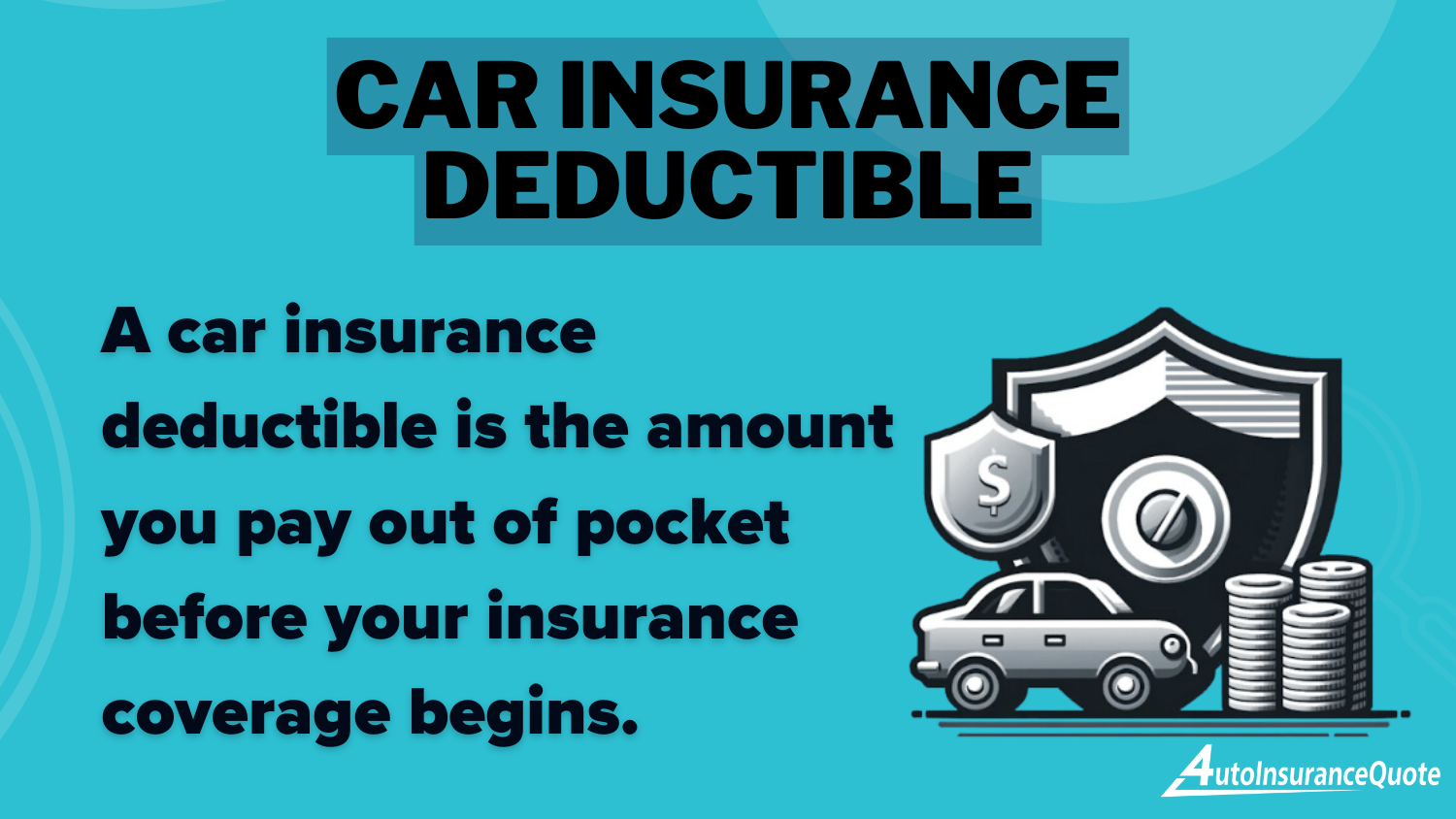

- 24–48 Hours: Contact your insurance agent. Provide the police report number and any photos of the damage. Be prepared to answer questions about the circumstances of the crash. Ask specifically about your deductible—if you are using your own collision coverage, you will be responsible for your deductible, even if you are not at fault.

Supporting Data: Coverage Costs and Financial Implications

Understanding the financial weight of your policy is essential before an accident occurs. Your choice of coverage directly dictates your out-of-pocket costs when you cannot hold another party liable.

Auto Insurance Monthly Rates by Provider & Coverage Level (Estimated Averages)

| Provider | Minimum Coverage (Monthly) | Full Coverage (Monthly) |

|---|---|---|

| Geico | $30 | $80 |

| USAA | $22 | $65 |

| State Farm | $35 | $95 |

| Progressive | $40 | $110 |

Note: These are industry-wide averages. Rates vary significantly based on your driving history, ZIP code, and vehicle type.

The "Full Coverage" Advantage: If you had chosen only the state-mandated minimum liability coverage, you would be paying for the entire repair bill out of pocket if you cannot identify the other driver. Full coverage (which includes collision and comprehensive) acts as a safety net, ensuring your insurer covers the repairs regardless of who is at fault, minus your deductible.

Official Perspectives: The Role of Liability

Insurance companies operate on the principle of liability. When you file a claim, the primary question for the adjuster is: "Who is responsible?"

When information is not exchanged, the burden of proof shifts heavily onto you. Licensed insurance producers, such as Dani Best, often advise clients that "Before filing an insurance claim, consider the extent of damage, your fault status, and whether it’s worth involving your insurer to avoid unnecessary complications and protect your coverage."

If the damage is minor—perhaps a scratched bumper that costs less than your $500 or $1,000 deductible—it may be more financially prudent to pay for the repairs yourself. Filing a claim, even if you are not at fault, can sometimes trigger a "rate increase" or "surcharge" depending on your state’s regulations and your insurer’s specific policies.

Implications of Failing to Report

Failing to handle an accident correctly carries legal and financial consequences. In many jurisdictions, including Florida and Texas, leaving the scene of an accident—even a minor one—can lead to non-criminal traffic infractions, fines, and points on your license.

Furthermore, if you fail to report the accident to your insurer in a timely manner, you lose the ability to use your own policy’s protections. An insurer may deny a claim if they determine that your delay in reporting prevented them from performing a proper investigation.

Understanding "Clean" Claims

A "clean" claim is one submitted with all necessary documentation, including:

- A valid police report.

- Clear, date-stamped photos of the vehicle damage.

- A detailed, consistent written narrative of the event.

Submitting an error-free claim drastically reduces processing time and prevents the back-and-forth communication that often leads to denied claims.

Frequently Asked Questions (FAQs)

What is the most common mistake after an accident?

The most significant mistake is leaving the scene without calling the police. Even if the accident seems minor, the lack of an official report makes it nearly impossible to prove the damage was caused by another party, effectively forcing you to file a collision claim under your own policy and pay your deductible.

Can I reverse an insurance claim?

Yes, in many cases, you can withdraw a claim before it is fully processed. However, if the insurer has already paid out for repairs or medical bills, you cannot simply "undo" it. Always consult with your agent before initiating a withdrawal.

How much do most settlements pay?

While averages vary wildly based on injuries and property damage, typical settlements for moderate accidents range from $15,000 to $30,000. However, in cases of minor property damage without injury, the payout is usually limited to the cost of repairs minus the deductible.

What if I am in a "No-Fault" state?

In "No-Fault" states, your own Personal Injury Protection (PIP) coverage pays for your medical expenses regardless of who caused the accident. This simplifies the process for injuries but does not cover vehicle damage. For vehicle damage, you will still need to rely on your collision coverage if the other party is unknown.

Proactive Protection: Final Thoughts

The stress of an accident is inevitable, but the financial fallout is manageable if you understand your policy. By maintaining a copy of your insurance ID card in your vehicle at all times, keeping a pen and paper handy, and knowing the limits of your coverage, you can transform a chaotic situation into a systematic insurance process.

Don’t wait until the next accident to find out if you’re underinsured. Take the time today to review your declarations page. If you are currently carrying only the state minimum, consider whether your financial situation could handle a significant repair bill. Using a free, secure comparison tool to review rates from top-tier providers is the most effective way to ensure you have the coverage you need at a price you can afford.

Disclaimer: This article provides general information. Insurance laws and policies vary by state and individual provider. Always consult your specific insurance policy or a licensed professional for advice tailored to your situation.